Payment Flows

This section provides an overview of available payment channels in Xenith. Each section describes what the payment method is and the typical customer flow.

🇧🇩 Bangladeshi Taka (BDT)

Ewallet

Overview

Customers can pay in BDT by transferring funds to a designated e-wallet account number displayed on the payment page. After completing the transfer, the customer must submit the Transaction ID for verification.

Payment Flow

- The customer initiates a payment request and is redirected to the payment page.

- The e-wallet account number is displayed on the payment page.

- The customer transfers the payment amount to the provided e-wallet account number.

- Once the payment is completed, the customer receives a Transaction ID.

- The customer enters the Transaction ID on the payment page. If the Transaction ID is valid, the transaction is approved within 30 seconds.

🇰🇭 Cambodian Riel & United States Dollar (KHR / USD)

Bank Transfer

Overview

Customers can pay by transferring funds directly in either KHR or USD using mobile banking or traditional bank channels.

Payment Flow

- Bank account details are displayed at checkout.

- The customer initiates a transfer using their banking method.

- The customer reviews and confirms the transfer.

- The payment is completed and the status is returned.

KHQR

Overview

KHQR is Cambodia’s standardised QR payment system by the National Bank of Cambodia. It allows customers to pay by scanning a single interoperable QR code using any supported banking or e-wallet app connected to Bakong.

Payment Flow

- A QR code is displayed.

- The customer scans the QR using a banking app or wallet.

- The customer reviews the payment details.

- The customer authorises the payment.

- The payment is completed instantly.

🇮🇳 Indian Rupee (INR)

UPI

Overview

UPI is India’s real-time payment system that allows customers to make payments using either a QR code or a UPI ID (VPA). Customers can complete the payment through any UPI-enabled app, such as GPay, PhonePe, or Paytm, by scanning the QR code or using the provided UPI ID.

Payment Flow

- The customer opens their UPI app (for example, GPay, PhonePe, or Paytm).

- The customer scans the QR code or copies and pastes the UPI ID (VPA) to make the payment.

- The customer authorises the payment in their UPI app.

- The customer returns to the deposit page and enters the UTR (Transaction Reference Number) to confirm the payment and complete the order.

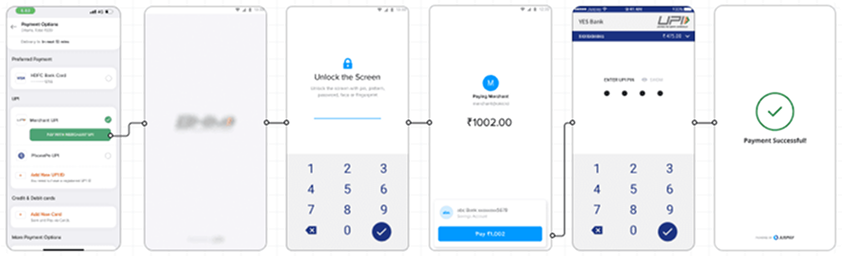

Intent

Overview

UPI Intent is a payment flow designed for mobile apps and web browsers that allows customers to initiate UPI payments directly from a merchant interface, triggering a redirection to a supported UPI app (e.g., Google Pay, PhonePe, Paytm) without requiring manual entry of a UPI ID or scanning a QR. It creates a more frictionless and mobile-first experience, increasing conversion rates and reducing drop-offs. The merchant app/web redirects the user with pre-filled transaction details, and the UPI app handles authentication and payment confirmation.

Payment Flow

- A list of supported UPI apps is displayed.

- The customer selects a UPI app and is redirected to it.

- The customer reviews the pre-filled payment details.

- The customer authorises the payment using a UPI PIN.

- The customer is redirected back with the payment status.

- The payment is completed.

image by juspay.io

🇮🇩 Indonesian Rupiah (IDR)

Virtual Account (VA)

Overview

A Virtual Account is a unique bank account number generated for each payment. Customers transfer funds to this number, and the payment is automatically identified and confirmed.

Payment Flow (Intrabank)

-

A unique VA number is displayed.

-

The customer initiates a transfer via mobile banking, ATM, or branch.

-

The customer reviews the payment details.

-

The customer confirms the transfer.

-

The payment is completed and automatically identified.

Payment Flow (Interbank BCA via INA Perdana)

Transfer via BCA Mobile

- Open the BCA Mobile application.

- Select m-Transfer.

- Choose Daftar (Register) > Antar Bank (Interbank).

- Enter the beneficiary account number and select Bank INA Perdana as the destination bank.

- After registering the beneficiary, go to Transfer > Antar Bank.

- Select Bank INA Perdana and choose the newly registered beneficiary account.

- Enter the deposit amount you wish to transfer.

- Choose the transfer network: BI-Fast or Realtime Online.

- Tap Send.

- Confirm the transfer, then enter your Transfer PIN and select OK.

- For transfers above Rp 250,000,000, please use RTGS.

- If you have previously transferred to Bank INA through BCA Mobile, you may start from Step 5.

Transfer via myBCA

- Open the myBCA application.

- Select the Transfer menu.

- Choose Transfer to Other Bank.

- Select Transfer to New Beneficiary.

- Search and select Bank INA Perdana.

- Enter the VA number in the Beneficiary Account Number field.

- Enter the transfer amount, select BI-Fast, then tap Continue.

- Review your transaction details; if everything is correct, tap Continue.

- Your transfer is complete.

- For transfers above Rp 250,000,000, please use RTGS.

Transfer via BCA ATM

- Insert your BCA ATM Card.

- Enter your 6-digit PIN, then press Enter.

- Select Transfer.

- Choose Interbank Transfer.

- Select INA PERDANA (Bank Code: 513).

- Enter the beneficiary account number.

- Enter the amount you wish to transfer.

- Review all transfer details; if correct, press OK to confirm.

Transfer via BCA Internet Banking (KlikBCA)

- Log in to KlikBCA.

- Go to Transfer > Antar Bank (Interbank).

- Select the transfer network: BI-Fast or Realtime Online.

- Choose INA PERDANA as the destination bank.

- Enter the beneficiary account number.

- Enter the transfer amount and ensure your balance is sufficient.

- Select your Transfer Fee Payment option.

- Review the transaction details, then click Send or Agree.

- You will receive a confirmation and proof of transfer.

QRIS (Quick Response Code Indonesian Standard)

Overview

QRIS is Indonesia’s standardised QR payment system. Customers scan a single QR code using their banking or e-wallet app to complete the payment.

Payment Flow

- A QR code is displayed.

- The customer scans the QR using a banking app or wallet.

- The customer reviews the payment details.

- The customer authorises the payment.

- The payment is completed instantly.

E-Wallets

Overview

E-wallets enable customers to make digital payments using apps like OVO and DANA through in-app authentication.

Payment Flow

OVO

- A payment prompt appears in the OVO app.

- The customer opens the OVO app to view the request.

- The customer reviews the payment details.

- The customer authorises the payment using an OVO PIN.

- The payment is completed, and confirmation is shown in the OVO app.

DANA

- The customer enters their phone number in the DANA page.

- A payment request is sent to the DANA app.

- The customer opens the DANA app when the prompt appears.

- The customer reviews the payment details.

- The customer authorises the payment using a PIN or biometrics.

- The payment is completed, and the status appears in the DANA app.

🇯🇵 Japanese Yen (JPY)

Bank Transfer

Overview

JPY Bank Transfer is a payment method where customers complete a payment by transferring funds directly to the provided bank account. The payment page displays the deposit amount, reference ID, bank account details, and payment instructions so the customer can complete the transfer accurately.

Payment Flow

- The customer initiates a payment to the provided bank accounts.

- The customer makes a bank transfer to the provided bank account number.

- Once the payment is completed successfully, the transaction status is updated to Success.

🇱🇦 Laotian Kip (LAK)

LAOQR

Overview

LAOQR is Laos’ national QR code payment standard, launched by the Bank of the Lao PDR to support convenient, safe, secure, and cashless domestic payments. Customers can scan a LAOQR code using a participating mobile banking app or wallet to pay merchants directly via QR code.

Payment Flow

- The customer scans the LAOQR using a participating banking app or wallet.

- The customer reviews the payment details.

- The customer authorises the payment.

- The payment is completed and the transaction status is updated to Success.

🇲🇾 Malaysian Ringgit (MYR)

DuitNow QR

Overview

DuitNow QR is Malaysia’s national QR payment standard. Customers scan the QR code using participating mobile banking apps or e-wallets to complete payment.

Payment Flow

- A QR code is displayed.

- The customer scans the QR using a banking or wallet app.

- The customer reviews the payment details.

- The customer authorises the payment.

- The payment is completed instantly.

Direct Debit FPX

Overview

FPX is Malaysia’s online banking payment method that connects directly to participating banks. Customers authenticate and confirm payments using their bank credentials.

Payment Flow

- The customer logs in using their bank account details.

- The customer reviews the payment details.

- The customer authorises the payment.

- The payment is completed and the status is returned.

🇵🇭 Philippine Peso (Peso)

E-Wallets

Overview

E-wallets enable customers to make digital payments using apps like PayMaya and GCash through in-app authentication.

Payment Flow

GCash

- A QR code is displayed.

- The customer scans the QR using their GCash app.

- The customer reviews the payment details.

- The customer authorises the payment.

- The payment is completed instantly.

Pay Maya

- The customer logins into their Pay Maya account.

- An OTP is sent to the customer.

- The customer enters the OTP and authorises the payment.

- The payment is completed, and the status appears in the Pay Maya app.

🇹🇭 Thai Baht (THB)

PromptPay QR

Overview

PromptPay QR allows customers to make payments by scanning a QR code via supported Thai banking apps. The transaction uses Thailand’s PromptPay network.

Payment Flow

- A QR code is displayed.

- The customer scans the QR using a banking app.

- The customer reviews the payment details.

- The customer authorises the payment.

- The payment is completed instantly.

🇻🇳 Vietnamese đồng (VND)

VietQR

Overview

VietQR is a QR-based payment method supported by Vietnamese banks. Customers scan the QR code using their mobile banking app to complete a payment instantly.

Payment Flow

- A QR code is displayed.

- The customer scans the QR using their banking app.

- The customer reviews the payment details.

- The customer authorises the payment.

- The payment is completed instantly.

Updated about 7 hours ago